July 15, 2026 | Read online

The Latest in ABS and Debt Markets

Welcome to The Data Tapes—your biweekly snapshot of private credit and ABS markets. In each edition, we bring you concise updates on debt financings, platform fundraises, data insights, market trends, and the latest from Setpoint.

🚀 What’s New at Setpoint

🆕 What we built in Q2: Firms leading in asset-backed finance are replacing manual systems with purpose-built technology to make decisions faster and scale more efficiently. See what we built in Q2 to support them.

💸 Debt Financings & Acquisitions

AI, Infrastructure & Energy

Brightspeed, a telecom and ISP platform owned by Apollo, plans to raise an asset-backed financing facility secured by subscription cash flows from its fiber network.

Linea Energy, a US-based renewable energy developer and IPP sponsored by EnCap Investments, closed a tax equity financing with Crux for its Watertown solar project, a 172 MWdc utility scale solar energy facility.

nScale, a London-based AI hyperscaler, closed a £672.3M revolving credit facility from a bank syndicate including JPMorgan, Goldman Sachs, and Morgan Stanley.

Williams, an energy infrastructure company, signed a JV with Blackstone and KKR to support the development of its five behind-the-meter power innovation projects, where Blackstone and partners will commit $5.34B in exchange for a 49% noncontrolling equity interest in the five projects.

Aviation, Rail & Transportation

AIP Capital, an alternative asset manager, is preparing to service its inaugural ABS issuance, a $643M deal secured by lease revenue on 18 aircraft.

Dubai Aerospace Enterprise, a global aviation services company, and Neuberger Specialty Finance launched Mustang Aerospace, an aircraft leasing co-investment vehicle that will invest ~$6B in aircraft assets over the medium term across multiple vehicles.

EasyJet, a British low-cost airline, received a competing acquisition offer from Apollo of £5.7 billion, competing with Castlelake’s prior £5.5 billion offer.

Real Estate & Mortgage

400 Capital, an alternative asset manager, closed capital relief transactions referencing a $1.5B residential mortgage loan portfolio on a US bank’s balance sheet.

Alterra IOS, an industrial outdoor storage (IOS) acquisition platform, closed a $400M refinancing led by Truist and KeyBank, secured by a portfolio of 99 IOS properties.

Brocc Finance, a Swedish credit platform, completed the acquisition of the remaining 35% minority interest in unsecured NPL portfolios previously held through a JV between Brocc and Intrum AB.

Fidelis, a real estate asset manager, is preparing to raise $191.5M in a new ABS issuance backed by revenues from RTL loans acquired from other RTL originators in its 4th rated deal.

Figure, a blockchain-native capital markets platform and HELOC originator, priced a private offering of $600M of senior notes used to finance the Kiavi acquisition.

Hope Capital Property Finance, a UK-based real estate lender, closed a £75M senior credit facility with TriplePoint.

MS Lending Group, a UK-based real estate investment firm, closed a £230M funding line with Pollen Street.

Auto & Consumer Finance

Addi, a Colombia-based BNPL platform, raised an $86M Series D financing led by Citius, with participation from BTG Pactual, GIC, and Monashees.

Consumer Portfolio Services, a consumer auto finance platform, renewed its credit agreement with Citi and its subordinate lender, increasing capacity to $508M. CPS also closed a $716.8M ABS issuance backed by a pool of auto loans for used vehicles.

Elevate, a digital consumer finance platform, closed a $655M credit facility led by Raven Capital, with participation from Hudson Cove and Bow River, to scale origination volume.

Fig Financial, a Canadian consumer fintech lender, announced it surpassed $500M in life to date originations since launching in 2023.

Klarna, a digital bank and payments platform, closed its first forward flow and warehouse facility in Germany, amounting to a €900M facility to scale originations in Germany.

Lendable, a UK-based digital lender, is raising £500M by selling securities backed by a portfolio of personal loans. Lendable has originated over £10B in consumer credit since launching over a decade ago.

Nexu, a Mexico-based auto finance platform, closed a $143M credit facility with HSBC.

Octane, a financial platform for recreational purchases, closed a $750M forward flow agreement with AB CarVal, with the option to upsize to $1.125B.

Oportun, a consumer finance platform, announced a lending partnership with Column to support Oportun’s unsecured personal lending program, where Column will originate loans on Oportun’s behalf.

Robinhood, a digital brokerage and banking platform, is looking to sell at least $400M in its inaugural ABS issuance secured by receivables from its Robinhood Gold credit card.

PayPal, a digital payments and lending business, received a joint bid from Stripe and Advent International to be acquired in a deal that would value PayPal at $53B. KKR is also marketing an ABS deal in Europe tied to PayPal’s BNPL business in Germany.

Upstart, an AI lending marketplace and consumer finance platform, closed a $569.4M ABS deal secured by auto-secured personal loans, third ABS deal of the year.

Commercial Finance

Elect Capital, a UK-based SME finance platform, closed a senior secured credit facility with Pollen Street.

Flex, a fintech platform for small businesses, closed a $70M Series B1 equity financing led by Halo Fund, the venture firm founded by Ryan Smith and Ryan Sweeney, at a $1.2B post-money valuation.

InKind, a software and financing platform for restaurants, closed a $320M financing with Liberty Mutual Investments who is serving as Senior and Mezz lender, to scale origination volume. InKind has provided over $600M in funding to restaurants since its 2014 launch.

Lendistry, a tech-enabled small business lender, closed a $100M credit facility from East West Bank to support Lendistry’s Airport Concessions Program which funds small businesses operating in airports across the US.

Mountain Ridge Capital, an asset-based commercial finance platform, upsized its asset-based lending facility with Wells Fargo Capital Finance to $400M.

Esoteric

Acacia Asset Management, a real estate investment firm, sponsored a securitization secured by a portfolio of 41,752 property tax lien assets, raising $235.7M.

Adams Outdoor Advertising, an out-of-home media company, closed a $765.1M ABS issuance backed by revenues from billboard advertising and related contracts.

Bending Spoons, an Italian acquisition and operating platform for digital platforms and mobile apps, went public with a $1.68B IPO under the ticker BSP.

CAA, a talent agency, partnered with TPG’s Integrated Media Company to form Compound Creative Holdings, a $250M holding company designed to acquire, operate, and grow a portfolio of Creator Economy businesses.

Insurance

Accelerant, a risk exchange platform for specialty insurance, announced a partnership with newly formed WoodStar Reciprocal Exchange, a reciprocal insurance company funded with $220M in surplus notes and capital from Kilter Finance, a KKR-backed specialty finance company.

💰️Platform Growth

Fundraises

Allianz closed $744M in commitments for the first close of Alliance Asian Pacific Secured Lending Fund III.

Artcos, a business of KKR, announced final close of $6.2B for Arctos Keystone Partners Fund I, a fund focused on bespoke growth capital and financing for alternative asset managers.

Cloud Capital, a data center investment firm, launched Cloud Capital’s Core Joint Venture Strategy, with Realty Income and Global Investor, seeded with three initial investments valued at over $6B.

Hayfin Capital raised more than €15B for its flagship direct lending strategy.

Incus Capital, a Spanish asset manager, had its second close on Europe Credit Fund V with €560 million in closed and committed capital.

Starwood Capital, a private investment firm, closed Starwood Distressed Opportunity Fund XIII with $10.2B in capital commitments to focus on real assets globally.

M&A

Russell Investments is being acquired by an investor group led by B Capital and CalPERS for $2.8B.

New Vehicles, Hiring & Structured Products

Churchill Asset Management, the US asset management company of Nuveen, and Seviora Holdings, Temasek’s asset management platform, closed a $400M collateralized fund obligation investing across Churchill’s US junior capital and private equity secondaries strategies, and Seviora’s Asian private credit and global fund of funds business.

GoldenTree closed a $726M CLO backed by a $710M portfolio of senior secured loans.

Seer Capital, a US-based hedge fund, is closing a $300M insurance-backed financing facility in partnership with Cantor Fitzgerald and Lockton to support SRT investments.

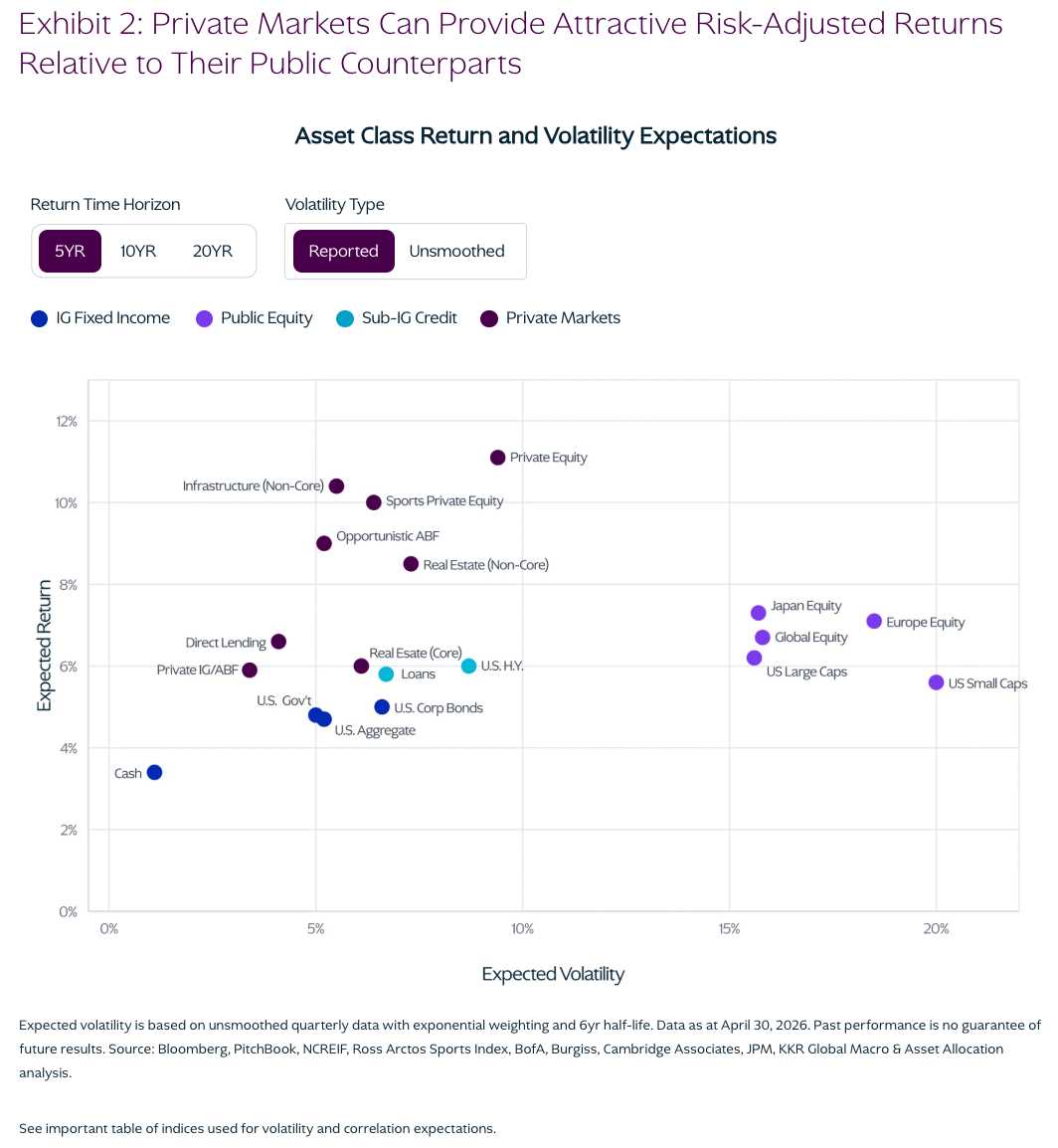

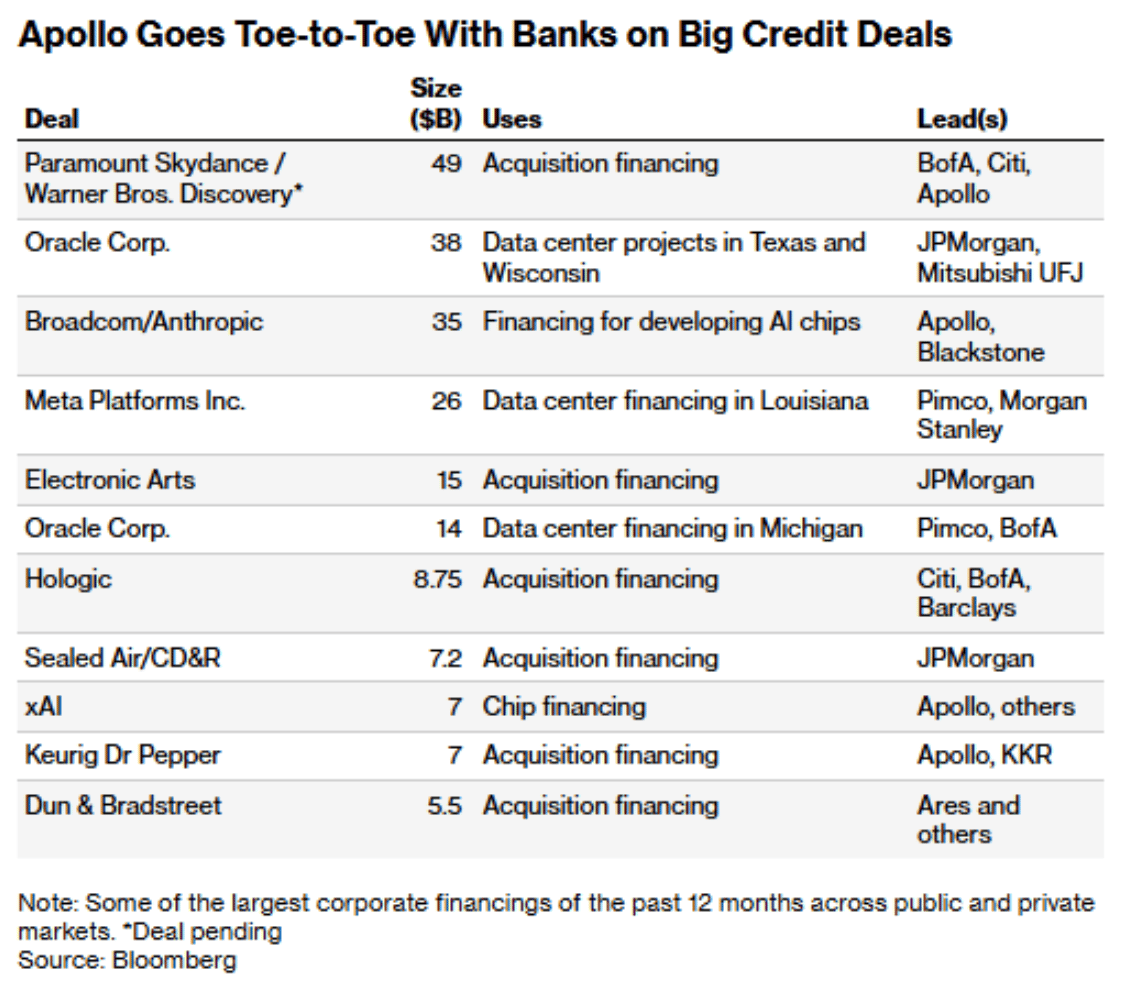

📈 Visuals

🗣️ Market Commentary

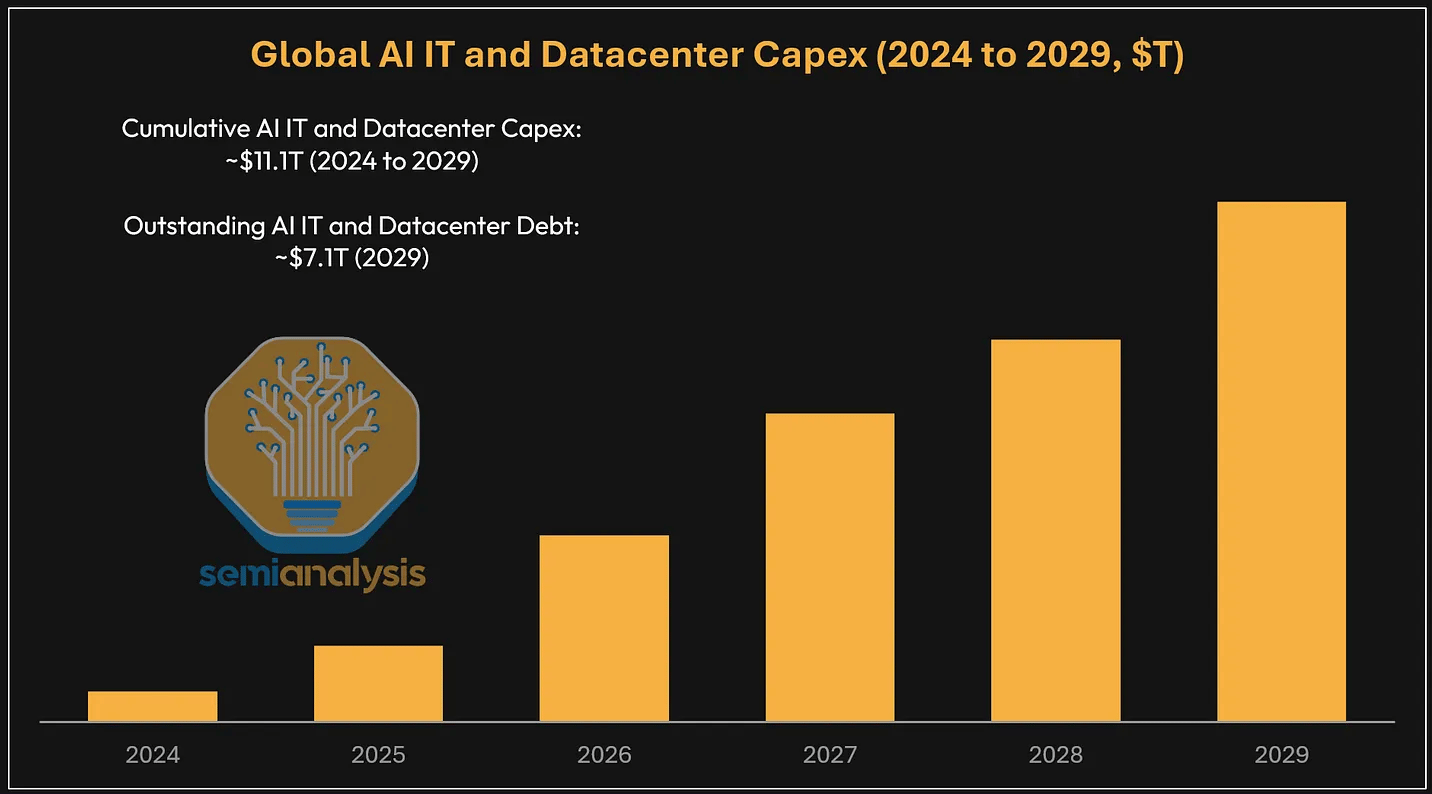

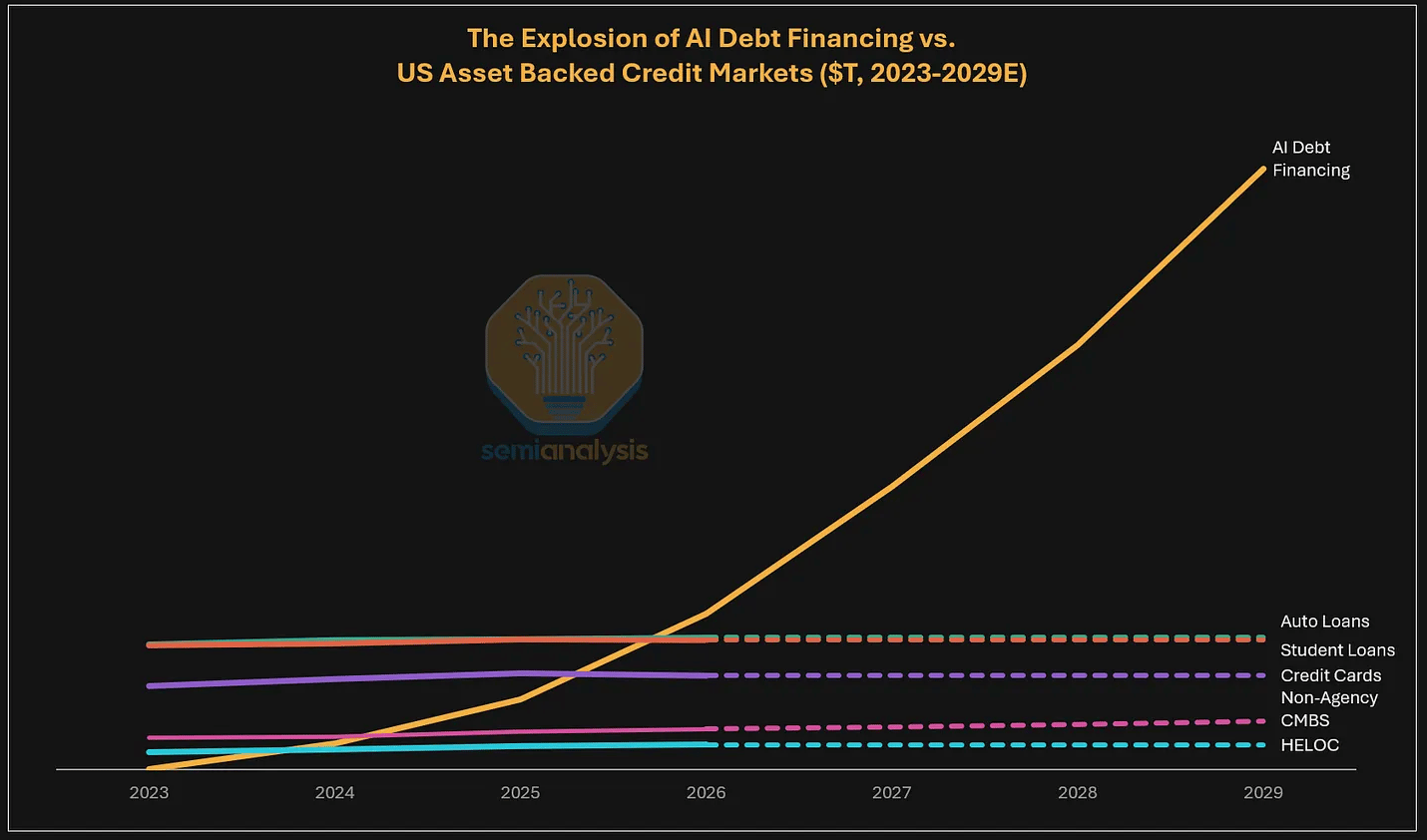

“AI Debt Financing will become a multi-trillion-dollar credit market, with over $7T of debt outstanding by 2029 driven both by AI IT Capex and AI Datacenter Capex needs for Neoclouds, datacenter builders, and even hyperscalers. This will make it the second largest asset backed debt market after the US mortgage-backed financing market at just over $13T. Annual AI Capex – including GPUs, networking, storage and attached CPU compute as well as for the Datacenters to house AI compute – will be well north of $2T in 2028. Cumulative AI Capex from 2024 to 2029 will reach ~$11.1T, and credit markets will be the main funding source for this buildout.” - SemiAnalysis on Market Size Estimates for AI Debt Financing

“The notion that somehow you can forever increase your operating leverage is a crazy notion. We don’t have that. I think it’s part of the reason why banks failed, if you go back 20 years ago. We’re never going to have that point of view. AI will have its gives and takes. We can’t project. I do think you might actually see a slowdown in growth, maybe a slowdown in 2027 or 2028. The teams are looking at all of our opportunities, and we pointed out over and over again when we have an opportunity to spend more money in marketing, with deposit ROI, we’re going to do it. We’re not going to have false gods. We have to pray that we can’t do something really smart.” - Jamie Dimon, JPMorgan CEO & Chairman on Limits to Operating Leverage in the Banking Sector

“It’s not a sensitive topic at all. We are going to use AI to do a better job for our clients. That’s our job. We fully expect it’ll have huge efficiency in certain parts of the company. We analyze it all the time. I think we’ve mentioned in the past, we spend quite a bit of money on it. We have a lot of MVPs that we know we have. The whole company’s working this at this point. I think there’s almost 1,000 use cases today, though we’d say that the really important ones are 50 across risk, fraud, marketing, hedging, prospecting, note-taking, idea generation, document reading. It’s kind of just starting. We do expect that. You can’t just say, “Well, your ROE is going to go to 50% and stay there.” If we had a 50% ROE and growing at 10% a year, we’d probably have, in 50 or 60 years, you’d probably be 100% of the GDP of the United States of America.” - Jamie Dimon, JPMorgan CEO & Chairman on AI Initiatives across the JPM

“In the case of prime, also in the case of FICC financing, as has been the case, there continues to be far more demand across the client segment than we’re willing to engage when we sort of balance our objectives of serving our clients, driving market share, but also being balanced, diversified and focusing on risk management. So we’re at a moment in time where the demands for the provision of financing are outstripping what we think is the appropriate quantum. That should come as no surprise. We are in the middle of an AI CapEx super cycle where there are demands on financing into every single financing instrument in every region of the world and across every single industry. So it’s a function of deploying our resources as efficiently as we can to serve our clients as best we can. But we’re at a moment in time where there’s more demand right now.” - Dennis Coleman, Goldman Sachs CFO on Supply vs. Demand for Prime & FICC Financing Businesses

📖 What We’re Reading & Listening To

Earnings & Investor Presentations

Reading

Capital Markets Assumptions (KKR)

Continuation Funds in 2026: Beyond Liquidity (Preqin)

Monitoring the AI Trade: Cross-Asset Risk Signals from Equity, Credit, and CDS (Apollo)

Nvidia GPU Debt Backstop Unleashes the AI Project Trinity: Capital, Offtake and Datacenters (SemiAnalysis)

Q2 2026 Alts Quarterly: Midyear Outlook (Brookfield)

State of the AI Economy (Exponential View)

The State of Private Credit in 2026 (9fin)

UK Challenger Banks Explore SRT Issuance to Manage Maturing Loan Portfolios (Octus)

Podcasts & Interviews

AI Dominates Economy and Markets with Torsten Slok (Steve Eisman)

The Future of Chips and Infrastructure with Dylan Patel (a16z)

Choosing Wisely: Where IC Invests and Where It Doesn’t (Flow of Funds with Glenn Schorr)

Julian Salisbury on Sixth Street’s Culture and Investing Across the Capital Stack (Money Maze)

The Blueprint Episode 7: Gregg Lemkau (Rockefeller Capital Management)