May 21, 2026 | Read online

The Latest in ABS and Debt Markets

Welcome to The Data Tapes—your biweekly snapshot of private credit and ABS markets. In each edition, we bring you concise updates on debt financings, platform fundraises, data insights, market trends, and the latest from Setpoint.

🚀 What’s New at Setpoint

Reflections from Private Credit’s Next Act: Setpoint and Blue Owl recently hosted a private panel discussion at a16z’s San Francisco office. Brad Stroh, Co-CEO and Founder of Achieve captured insights from the conversation. Read his piece here.

The Most Important Financial Institution Nobody Talks About Anymore: GE Capital was a $600B lending platform that shaped the ABF playbook Apollo, Ares, KKR, and others still run today. It’s been dead for five years, but its influence on the architecture of modern private credit is everywhere. More from Business Development & Partnerships Lead at Setpoint, Conor Witt, here.

Upcoming Events:

Capital Conversations Summer Kickoff — June 2: Join Setpoint and Cross River for Capital Conversations, a happy hour bringing together the asset-backed finance community in NYC. Apply to attend.

We’re on the road — let’s connect:

IMN’s Residential Mortgage Securitization, June 3 — New York, NY | Meet with us.

Global ABS, June 9-11 — Barcelona, Spain | Meet with us.

💸 Debt Financings & Acquisitions

Affirm, a consumer BNPL platform, expanded its long-term partnership with One William Street via a new dedicated OWS fund to purchase roughly $1.5B of loans through 2027, in addition to extending an existing facility to purchase an additional $500M per year in loans through 2027.

ALLO Communications, a fiber-optic telecom infrastructure platform, closed an $824.4M ABS issuance backed by contract payments from fiber optics networks.

Altriarch, an alternative asset manager, announced the acquisition of a $30M A/R factoring portfolio from a fintech-enabled specialty finance platform.

BIG Fiber, a dark fiber infrastructure provider, closed a $250M debt facility with an additional $100M accordion from Stonepeak Credit and La Caisse (fka CDPQ) to accelerate expansion in core markets.

Carvana, an online used car retailer, closed a $1.1B ABS issuance secured by a pool of fixed-rate, retail installment sale contracts on used vehicles.

CoreWeave, an AI hyperscaler, closed a $3.1B delayed draw term loan facility to support its AI cloud platform expansion from Morgan Stanley and Mitsubishi UFJ Financial Group.

Credibly, a small business finance platform, closed over $260M in new financing including a new securitization and the refinancing of its existing warehouse and mezzanine facilities with Truist Bank and Medalist Partners.

Crux, a capital platform for clean energy, closed a $500M debt financing facility with Nuveen Energy Infrastructure Credit to finance Crux-led tax driven investments including hybrid tax equity.

Diversified Energy partnered with Carlyle to acquire oil and natural gas properties in the Anadarko Basin from Camino Natural Resources for ~$1.2B. Carlyle’s Global Credit platform structured a bespoke ABS to finance the deal — a newly formed SPV holds the PDP assets and issues debt backed by the underlying cash flows, with Carlyle holding a majority SPV stake and Diversified operating the assets.

Exponent, a financial platform for multi-location franchise operators, raised a $30M credit facility from Jovian Capital to scale its lending product alongside a $7.5M Series A financing.

Honor Capital, an insurance premium finance company, acquired Ascend, a financial operations platform for the insurance industry.

McGrath RentCorp, a business-to-business rental company, closed a $725M credit facility with a syndicate of banks including Bank of America, US Bank, and Wells Fargo.

Mercury, a neobank for SMBs, raised a $200M growth equity round from TCV, Sequoia, a16z, and Coatue at a $5.2B valuation.

Octane, a financial platform for recreational purchases, closed a $350M forward flow agreement with Nuveen in a one-year arrangement to purchase fixed-rate installment powersports and outdoor power equipment loans.

Pagaya, a consumer finance and residential real estate platform, announced a partnership with Sezzle to embed Pagaya’s AI underwriting platform at point of sale to help more borrowers access installment loans.

Parafin, an embedded SMB finance platform, upsized its warehouse facility with SVB and brought in EverBank as a new A-note lender.

Regents Capital, a commercial finance platform, closed its inaugural securitization in a $132.9M issuance secured by a pool of loans and leases spanning a range of industries.

Relay, a banking and money management platform for SMBs, closed a $50M growth investment from General Catalyst’s Customer Value Fund to finance customer acquisition.

Ripple Prime, the institutional prime-brokerage unit of Ripple, closed a $200M asset-backed debt facility with Neuberger Specialty Finance to scale Ripple Prime’s margin lending and financing capacity.

Sankaty Jet Capital, a business aviation lending platform and wholly owned subsidiary of AIP Capital, closed a $68M committed secured mezzanine facility with Wheels Up Experience.

Scratch Financial, a payment processor and loan platform for veterinary clinics, closed a purchase facility with Victory Park to scale loan origination volume.

Sezzle, a consumer BNPL and payments platform, closed a new $300M receivables funding facility with Mesirow Alternative Credit, doubling the original commitment from 2024.

Splitero, a home equity investment platform, closed a $275M ABS issuance secured by a portfolio of 2,246 fixed home equity investment agreements in a deal sponsored by Splitero and BOAC HOWL Splitero Securitization Holdings.

Westlake, a technology-based auto finance company, closed a $1.4B ABS issuance secured by a pool of subprime auto loans.

💰️Platform Growth

Abry Private Debt closed its acquisition of a $330M diversified private credit portfolio in partnership with Coller Capital.

Antares Capital closed its third Senior Loan Fund with $8.5B in total commitments.

Apollo is in talks to sell MidCap Financial Investment Corp, a publicly listed BDC, which Apollo values at roughly $3B.

Barings announced the close of over $19B in committed capital for its Global Direct Lending strategy.

Blackstone announced a JV with Google to create a US-based TPU cloud offering with $5B in equity commitments to bring 500 MW of capacity online in 2027.

Blackstone Real Estate Debt Strategies launched a lending platform to provide capital for homebuilders to enable construction of 50,000+ for-sale homes annually.

Corbin Capital announced the final close of Corbin Litigation Finance Fund I (CLF I) with $342M in committed capital to focus on commercial litigation funding opportunities.

CPP Investments announced its sale of remaining interests in its European NPL portfolio to a new JV managed by Arrow Global Group and Fortress.

D2 Residential, the multi-family credit platform run by D2 Capital, closed its first CRE CLO of $935.3M backed by 19 multifamily loans.

FGI Worldwide, a provider of working capital financing and trade credit insurance solutions, announced it has been acquired by Goldman Sachs Alternatives’ private equity business.

Flexpoint Ford raised $1.1B in initial closings for Asset Opportunity Fund III, its asset-backed credit strategy, and Insurance Opportunity Fund I, its insurance-sector vehicle.

HPS Partners announced a €15B Private Capital Program with Citi, a strategic collaboration to expand capital solutions and private financing to corporate and sponsor-owned borrowers in EMEA.

Monroe Capital closed Monroe Capital ML CLO XVIII, its latest $426.6M term debt securitization collateralized by a portfolio of lower and middle market senior secured loans.

Shamrock Capital, a media investment firm, raised $813M for Shamrock Capital Content Fund IV to identify, acquire, and actively manage media content and rights.

Stellus Capital Management, a lower middle market direct lending firm, announced the final close of Stellus Credit Fund IV with $1.5B in investible capital.

Stonepeak, an alternative investment firm focused on infrastructure and real assets, acquired BMO’s Transportation Finance and Vendor Finance businesses, including existing loan portfolios.

Värde announced the close of VMC 2026-FL6, a $1B managed CRE CLO made of up of a pool of 19 floating-rate mortgages secured by 40 commercial properties.

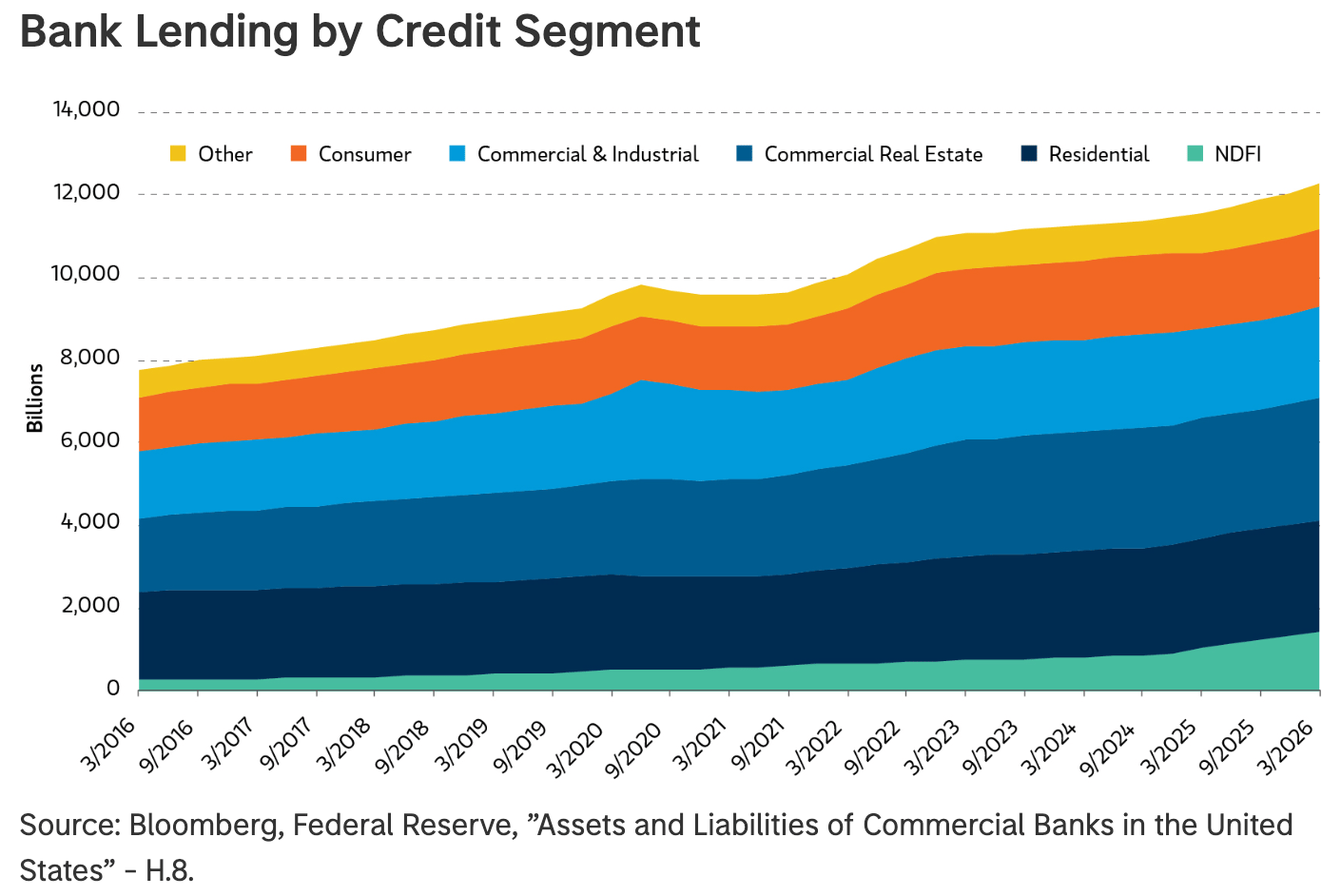

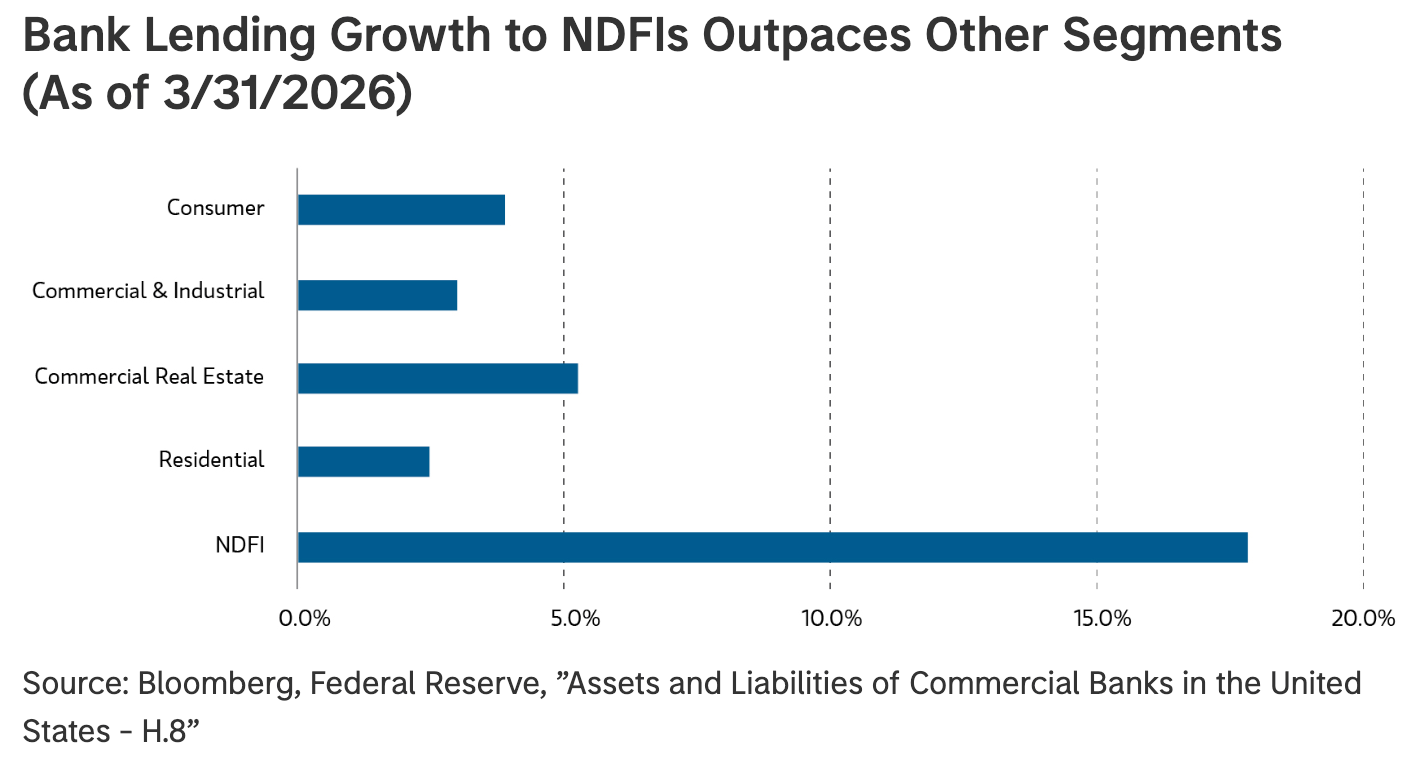

📈 Visuals

Source: Bessemer Venture Partners

🗣️ Market Commentary

“The [AI infrastructure capital requirement] numbers are massive, you’re absolutely right. This is the big question that every buyside investor is trying to get their grips around. There’s a couple of numbers out there. $5 trillion is the total hyperscaler capex over the next five years. If you think through what’s happened in Investment Grade so far, we’ve had $150B already this year. That same time last year was $20B. High yield, $40B this year. Same time last year, $0. So it really has become exponential in the volume we’re seeing.” - David DeBoltz, JPMorgan US Leveraged Finance Managing Director on demand for capital in the AI and Data Center ecosystem

“Perceived or actual stale valuations may create a first-mover incentive during stress events, leading investors to exit a fund before asset values are potentially marked down. Managers may have potential incentives to manage valuations of their funds in a way that minimises the appearance of volatility, such as by delaying or spreading out the impact of negative shocks that could reduce asset values.” — FSB, Report on Vulnerabilities in Private Credit, on valuation opacity and redemption dynamics

“PE-backed software, lenders took solace in the fact that you were a low loan--to-value. You would overlook high leverage multiples and would take comfort in the fact that someone was buying the business and you were lending at 40 cents on the dollar relative to the purchase price. At the end of the day, at 40% LTV, you might be 8-10x levered, all of your cash flows goes to support the debt service. When you have all of your cash flow supporting debt service you can’t invest in the future of the business.” - Tony Minella, CEO of Eldridge Capital Management, on the Pitfalls of LTV-Driven Underwriting in PE-Backed Software

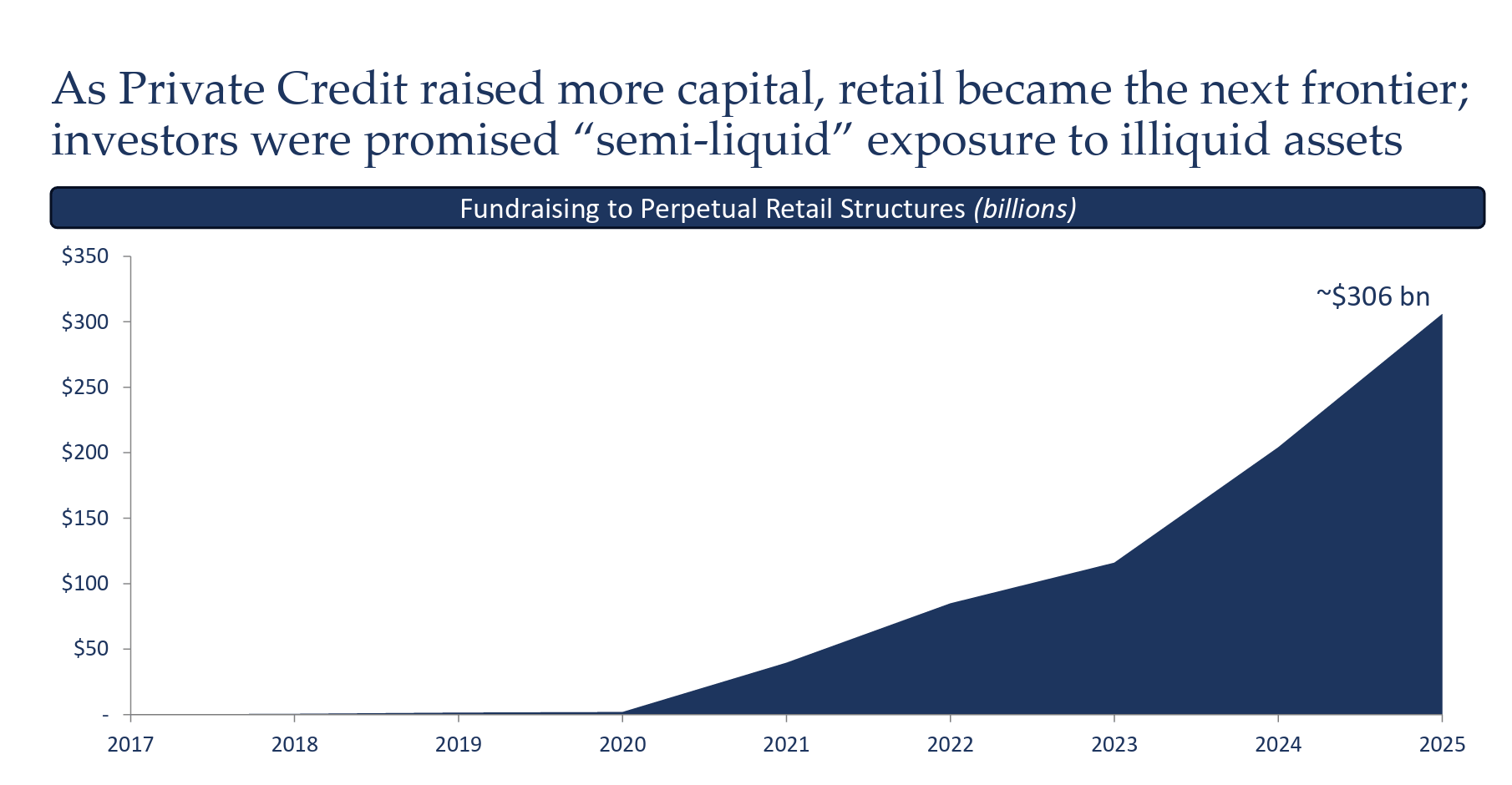

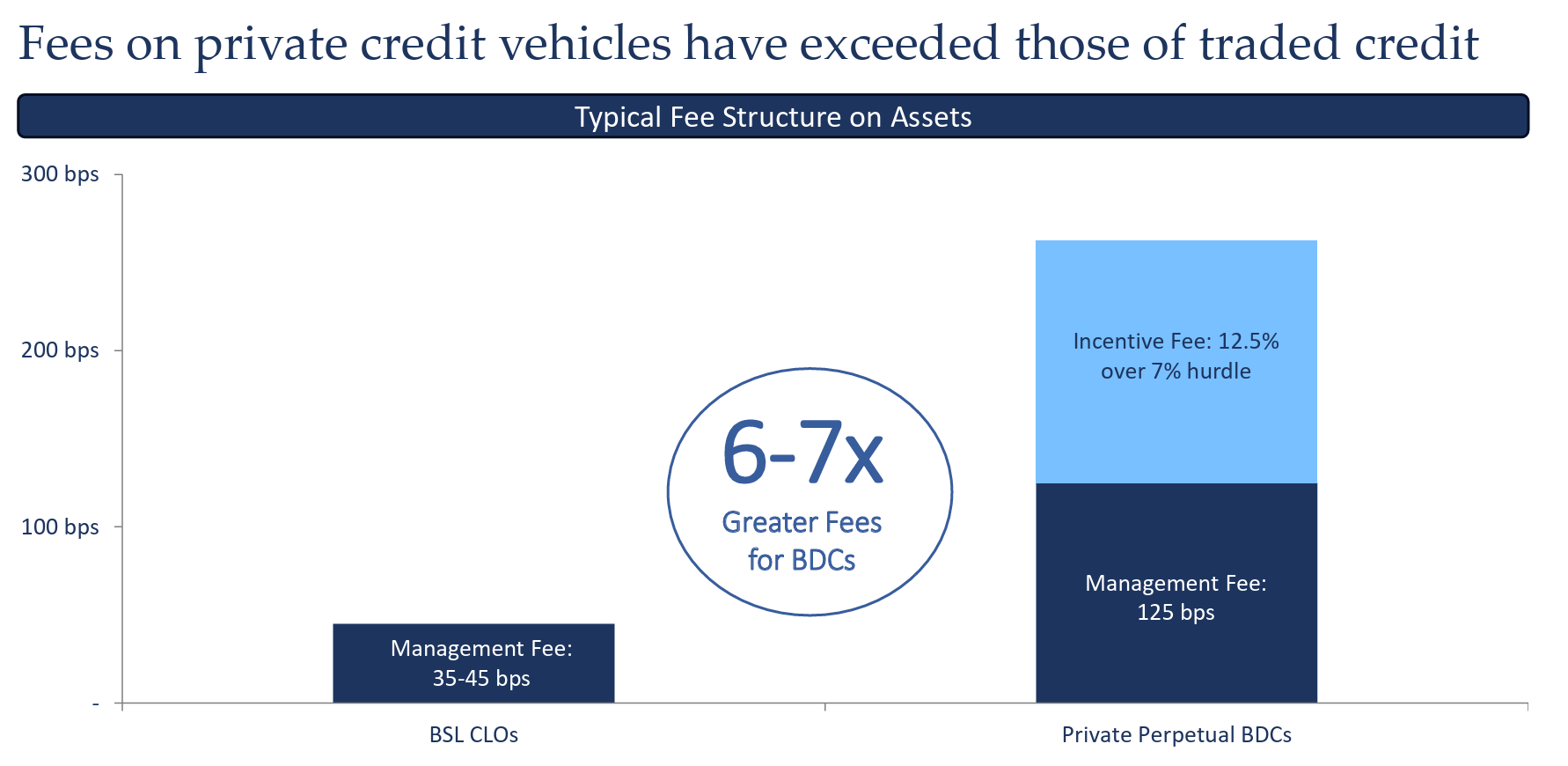

“More recently, semi-liquid private BDCs have been all the rage for public alts managers to raise. Promising liquidity in illiquid assets. $300B raised over the last 5-6 years. Why? Fees. If you can do a $1-2B unitranche deal and put a first lien and second lien into your CLO, you make 40 bps. Putting it into a private BDC, you make 6-7x that number. Why? FRE FRE FRE. Multiples expanded dramatically for public alts managers, driving their stocks higher, with a huge amount of the growth from private credit, from lev fin direct lending. M&A picks up. If you don’t own a private credit business, you have to buy one. When you have that much money to deploy and that much interest in the asset class and you have to raise more to drive your stock higher, how are you going to deploy it? You build an industrial scale deployment platform.“ - Scott Goodwin, Co-Founder and CIO of Diameter Capital Partners, on the Fee Incentives Driving Industrial-Scale Private Credit Deployment

📖 What We’re Reading & Listening To

Reading

AI Eats the World (Benedict Evans)

Dispersion Revisited (Oaktree)

Goldman-backed Lendable plots US expansion after outpacing banks on loans (FT)

The Crypto Borrowing Gap (Ledn & Protocol Theory)

Wall Street Takes Its Cut of $34 Trillion in US Homeowner Wealth (Bloomberg)

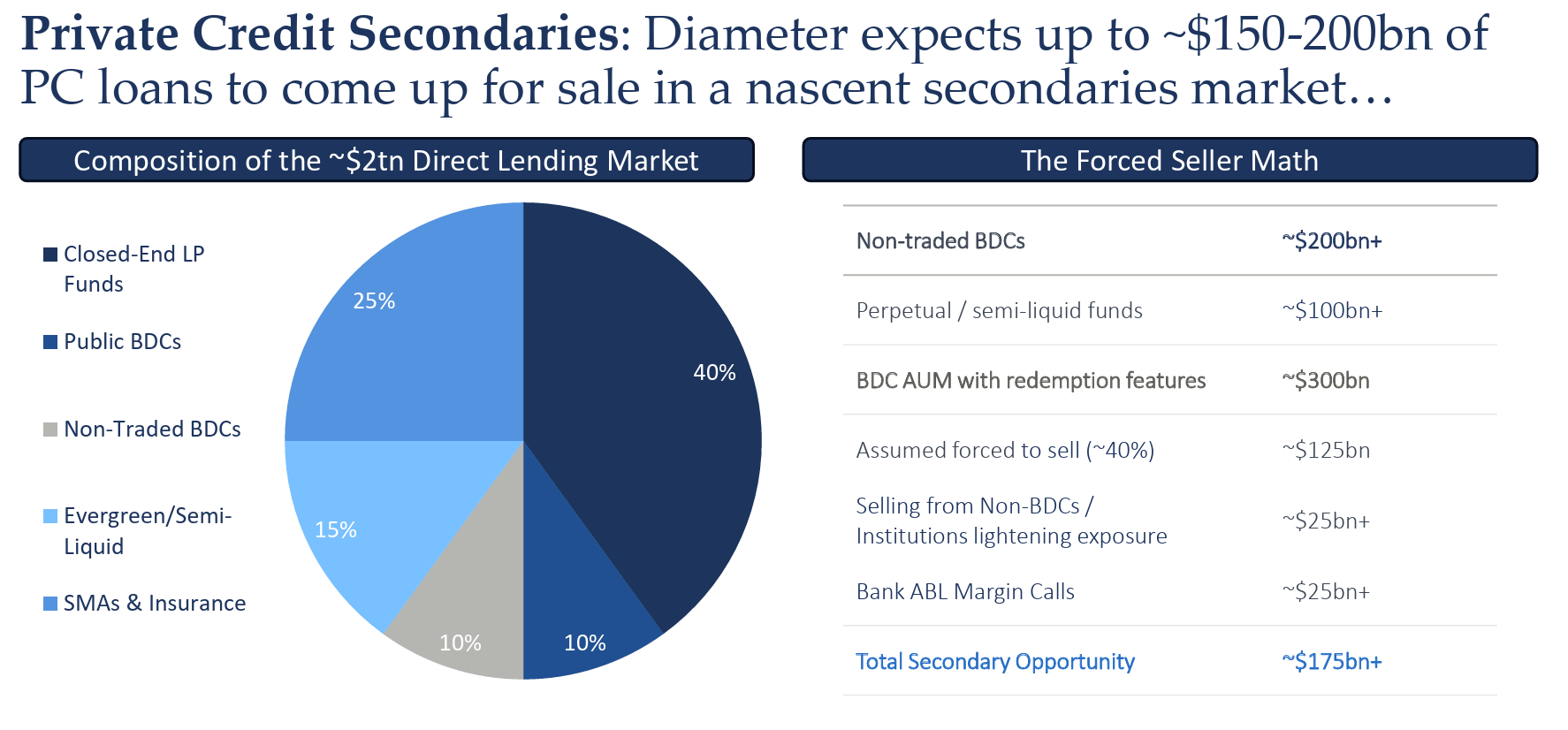

WTF Is Going On In Private Credit? (Diameter)

Podcasts & Interviews

Behind the AI Debt Boom, with David Deboltz from JPMorgan (Bloomberg)

CLO’s Explained: How they Work and What Drives Returns with Lauren Basmadjian (Flow of Funds)

Flight Path: Private Credit and Global Aviation Finance (AB CarVal: Uncommon Capital)

Oaktree’s Deputy CIO of Strategic Credit Milwood Hobbs Jr. (Credit Exchange)

Scott Goodwin presents at Sohn 2026 (Sohn Conference)

Conversation with BlackRock CEO Larry Fink & Brookfield Corp CEO Bruce Flatt (Milken Conference 2026)