March 04, 2026 | Read Online

The Latest in ABS and Debt Markets

Welcome to The Data Tapes—your biweekly snapshot of private credit and ABS markets. In each edition, we bring you concise updates on debt financings, platform fundraises, data insights, market trends, and the latest from Setpoint.

💸 Debt Financings & Acquisitions

Aspire Mortgage Trust, an RMBS securitization platform sponsored by Redwood Trust, closed a $391.2M ABS issuance secured by first lien-mortgages from multiple originators.

Avant, a Chicago-based consumer finance platform, closed a $200M ABS transaction with a AAA rating secured by a pool of unsecured personal loans originated through the Avant platform.

Bravo, a Spanish financial advisory and debt management platform, closed a €200M credit facility with Fortress to accelerate the development of its credit operation.

Broadleaf Financial Group, a specialty finance company focused on equipment leasing and financing, closed a new warehouse facility with Deutsche Bank to scale origination volume.

CAN Capital, a small business finance platform, acquired the equipment finance portfolio of Republic Bank Finance, a division of Republic Bancorp.

CoreWeave, an AI hyperscaler, is in market to raise $8.5B from MS and Mitsubishi UFJ Financial Group to finance the buildout of of cloud computing capacity for Meta.

DailyPay, an earned wage access platform, closed a $200M upsize of its secured credit facility to bring total capacity to $960M.

Fundbox, a US-based small business finance platform, closed a forward flow facility with Mesirow Alternative Credit. Fundbox also expanded its credit facility with ATLAS SP and Blue Owl.

FundingCircle, a UK-based SMB finance platform, closed a £700M forward flow with Waterfall Asset Management, expanding their existing partnership with senior financing from Citi.

Genesis, a Dublin-based commercial aircraft leasing platform, entered into a partnership with Flexpoint Ford to acquire and service a portfolio of commercial aircraft on behalf of Flexpoint. Genesis also closed a $90M credit facility with DB to strengthen its funding platform.

GoldState Music, a music-focused investment platform, closed a partnership with BridgePoint Group to invest in profitable music-oriented businesses across the music value chain.

Gracie Point, an insurance-focused specialty finance platform, closed a $250M warehouse facility with Goldman Sachs to scale insurance premium finance originations.

Inhale Capital, a UK-based bridge lending platform, closed a £50M senior revolving credit facility with TriplePoint to scale originations.

Homestead Capital, an investor and owner of farmland assets in the US, closed a $300M asset-based finance program with Barings to expand loan origination.

Keystone National Group, a Utah-based credit fund, closed a $44M credit investment via a senior secured credit facility for a specialty finance company.

Ledn, a Cayman-based bitcoin-backed lending platform, closed its inaugural ABS issuance of $188M secured by a portfolio of bitcoin-collateralized loans.

Lendbuzz, an auto finance platform, closed a $246M ABS issuance secured by a pool of auto loans for new and used autos, light duty trucks, and vans, marking its 11th public securitization.

Marathon Asset Management, a global asset manager, closed a $615M aircraft securitization secured by a portfolio of 27 Airbus and Boeing narrowbody aircraft on operating leases.

MEP Capital Management, a media-focused investment firm, took a majority stake in BondIt Media Capital, an independent film and TV financing platform, alongside a new $100M credit facility.

Morgan Stanley Investment Management, through its AIP Alternative Lending Group, closed its first pre-funded securitization of $220M secured by a portfolio of consumer loans from multiple originators.

Navient, a student loan finance company, closed a $683M ABS deal secured by a pool of refinance student loans.

North Mill Equipment Finance, a commercial equipment finance platform, closed a $440M ABS issuance backed by a pool of equipment loans and leases.

Onslow Bay, a mortgage finance company and RMBS aggregator, closed a $452.7M ABS issuance secured by a pool of first and second-lien revolving HELOCs.

Point, a home equity investment platform, closed a $346.4M ABS issuance secured by a pool of home equity investment agreements.

Propel Holdings, a Toronto-based consumer finance platform, closed a $60M forward flow purchase agreement with Mesirow Alternative Credit to finance originations through Freshline.

Purchasing Power, an employee benefit program provider, closed a $225M ABS issuance backed by a pool of consumer receivables originated from Purchasing Power’s payroll purchase platform.

Service Properties Trust, a Boston-based REIT with $10B in investments closed a $745M ABS deal secured by a pool of net lease mortgage notes.

SME Finance and Leasing Solutions, an Irish nonbank lender, closed a €100M credit facility with Pollen Street to finance originations to Irish small and medium enterprises and farmers.

Upstart, a consumer finance platform, closed a $333M bulk sale of auto loans to Bayview. Upstart also closed a $200M forward flow with Wafra to sell auto loan assets originated through Upstart.

Vero Finance Technologies, a SaaS and servicing platform for floorplan financing, closed a partnership with CIM to launch an EV floorplan financing program.

Wayflyer, a Dublin-based working capital provider for small businesses, closed a $250M credit facility with ATLAS SP to finance originations.

Yendo, a vehicle-secured credit card, closed a $200M committed credit facility with i80 to finance new credit card originations.

YouLend, an embedded financing platform for e-commerce, payment, and technology platforms, closed a $225M forward flow agreement with Värde.

💰️Platform Growth

Brookfield acquired Ori Industries, a distributed AI cloud platform offering on-demand access to GPU compute.

Nuveen to buy Schroders Plc in a £9.9B acquisition, creating a $2.5T AUM asset manager.

Oaktree closed $2.4B in commitments for Oaktree Special Situations Fund IV.

Saluda Grade hires Patrick Lo, formerly Co-CIO of Waterfall, to join the firm as Co-CIO to lead expansion into a broader range of asset-based finance capabilities.

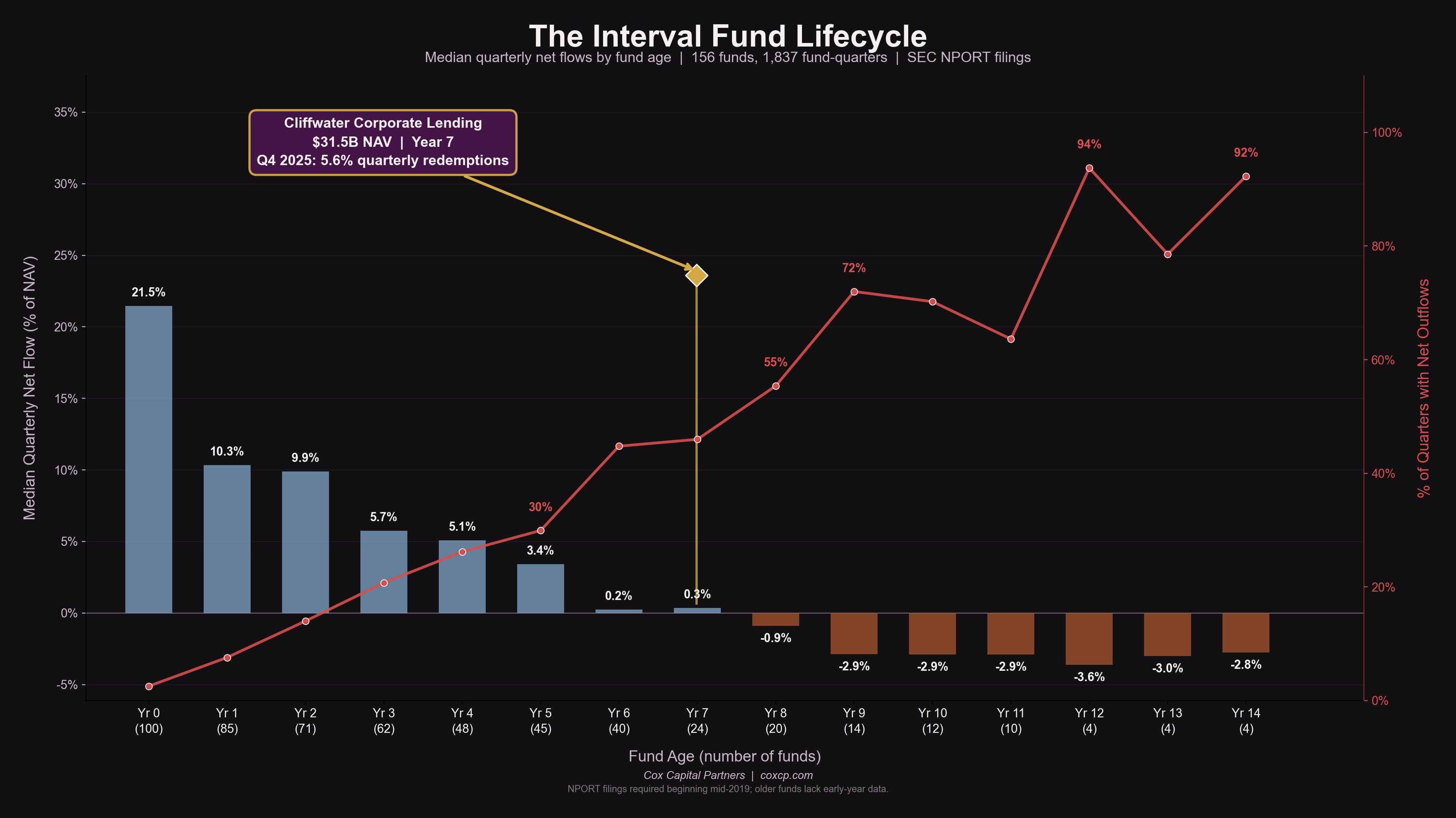

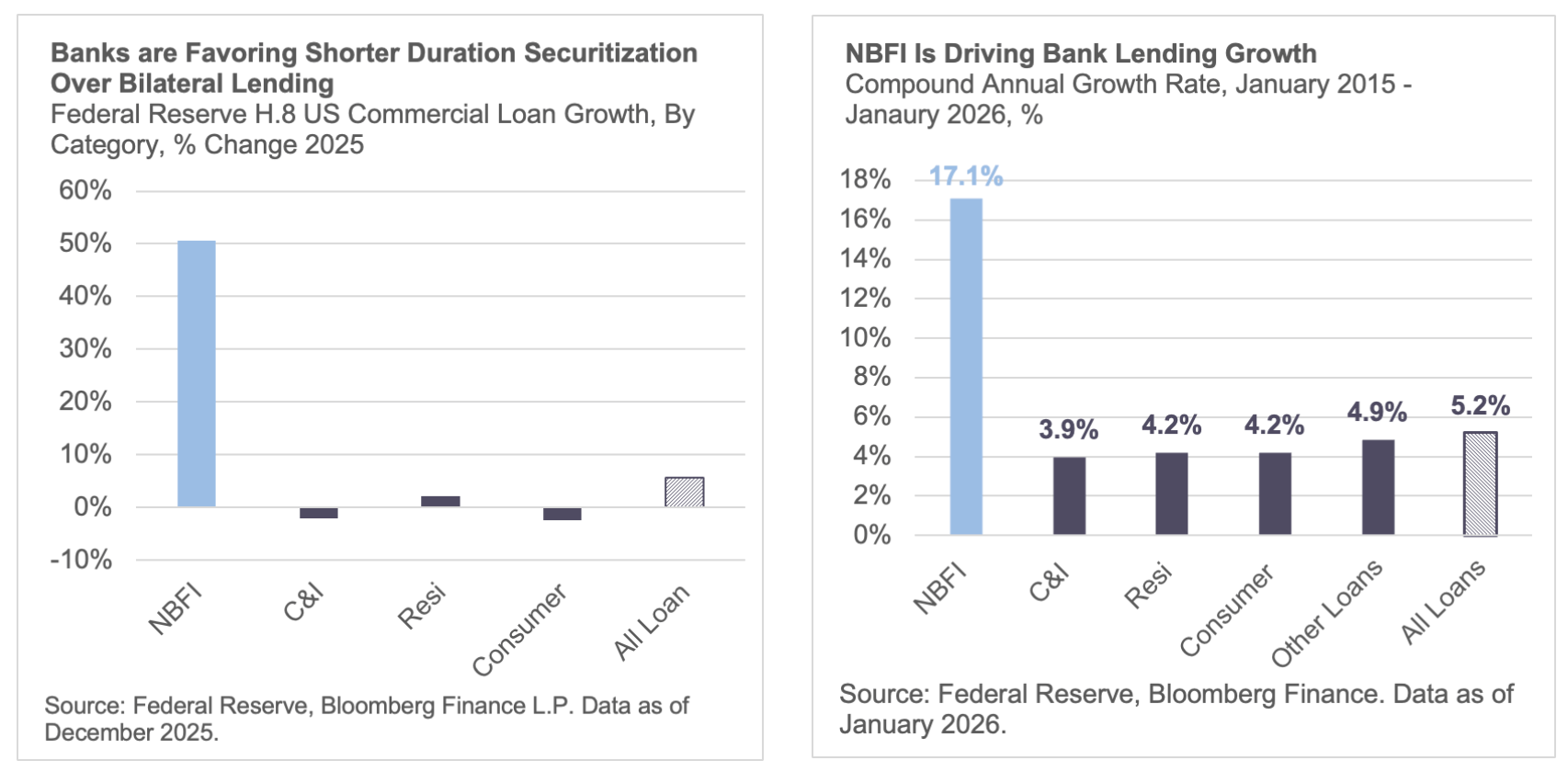

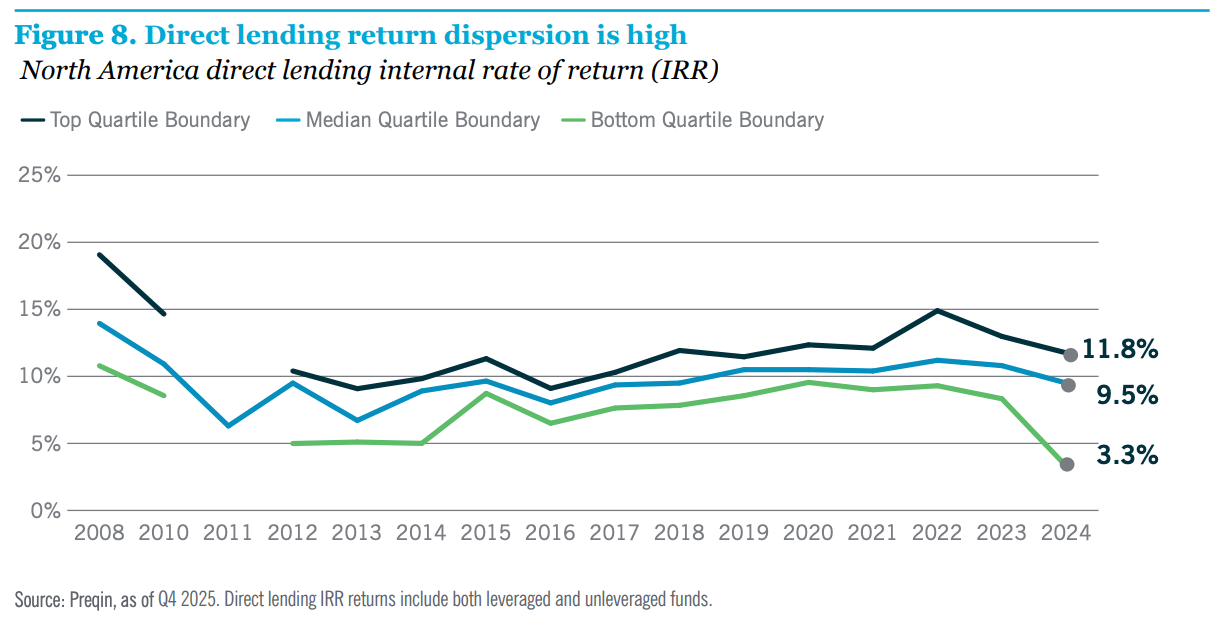

📈 Visuals

🗣️ Market Commentary

“With rising redemptions and limited liquidity, private BDCs and intervals funds are facing one of their toughest periods yet – leaving many investors with limited options. To help retail investors navigate this challenging period, today Saba and Cox Capital Partners announced our intent to offer liquidity for OBDC II, OTIC and OCIC shareholders through tender offers, subject to certain terms & conditions and the number of shares to be purchased.” - Boaz Weinstein, Founder & CIO of Saba Capital Management on Proposed Tender Offer to investors in 3 Blue Owl BDCs to buy shares at 20-35% below recent NAVs.

“One has to worry about opaque assets where there’s illiquidity,” he said in the interview airing Sunday. “We’re getting close to the end of late stages of cycles on this — and we’re due for a kind of a reckoning.” - Lloyd Blankfein, former CEO of Goldman Sachs on Impending Corrections in Financial Markets

“What we’re seeing now is banks trying to reduce their exposure across some of their data center names, not because of risk, not because of fears. Because they want to buy more. Because they’re already at capacity issues. Because the opportunity set is so big. So I do think the thing that is going to happen is frankly, if you think about the power demand that’s needed as well as the power demand that’s needed, I don’t know that it’s fully achievable to the levels that have been modeled in. I do think you’re going to hit a bit of a wall because of power. You’re going to hit a wall because of the sheer capital that’s supposed to be there to finance that piece. So right now, there’s this huge demand, and there’s a lot of different projects. I think you’ll see a slowdown of that because I think it’s probably unsustainable for the sheer amount of capital, financing, and power that needs to go into these projects. The power is going to become more of a problem than the data centers.” - Joel Holsinger, Co-Head of Alternative Credit at Ares on Current Dynamics and Demand Drivers in Data Center Financing

“Will AI affect some companies and will some companies or loans to some companies not pan out as expected or multiples paid too high for businesses. Yes, that happens in every cycle. This is not that big of a deal for the financial system. That’s the most important thing that the news is overlooking. People are worried about change - we’re going through faster changes today than we’ve ever gone through before. But I would go back. We’ve been building the backbone of the global economy for 40 years. The types of things we’re building are just different. Before it was water systems, pipelines, toll roads. Then it was telecom towers. Now it’s data centers and AI factories. The backbone evolves. I think people just get unsettled by that.” Bruce Flatt, Brookfield CEO on Overblown Concerns on Software, Private Credit, and AI Infrastructure Expansion

“Here’s the big takeaway to think about. As it relates to public credit markets, only 3% of the high yield market in the US is software. So that’s in really good shape. In the BSL market, which is also a liquid credit market, its 13% exposure. Probably manageable, but will be under pressure. In the private credit market, it has 23% exposure. In the public equity markets in the S&P 500 and Russell 2000, only 7% of the companies are software companies. If you’re a private equity manager or private credit manager and you have less than 10% exposure, I think you adjust the market and you’re perfectly fine. But if you have 23% exposure which is actually the number for private credit exposure to software companies, you’re having a lot of pain right now and you’re going to have to deal with a lot of fallout from this. At the end of the day there will be two types of software companies. Software is going to survive and do quite well overall. But the multiples that they trade at have contracted and they’ll probably stay contracted until we can sort out the winners from the losers. The winners will see the creative destruction from AI allow it to sort to new values that are much greater than what we see today. But the fallout is that companies won’t survive this because it’s not creative destruction, it’s just destruction. That will be very problematic. In credit, here’s the problem. In the public equity markets, the companies aren’t very levered. They’re only a half a turn of leverage which means they’re less than 1% debt-to-ebitda net of cash. But in the private credit markets they’re 10x levered. So any type of problem with debt financing is a real problem.” - Bruce Richards, Marathon Asset Management founder & CEO on Software Exposure in Private Credit and Leverage Disparities between Public and Private Software Businesses

📖 What We’re Reading & Listening To

Investor Letters & Outlooks

AI Hurtles Ahead (Oaktree)

Ares Annual Letter (Ares)

Brookfield Letter to Shareholders (Brookfield)

The Total Approach: A Practical Framework (KKR)

Reading

FY2025 Secondaries Market Overview (Campbell Lutyens)

MFS Creditors Warn of £930 Million Shortfall in Collateral (Bloomberg)

Opportunistic Credit as a Complement to Direct Lending (MidOcean Partners)

Private Markets Hiring Defies Gloom with $2.5M Pay Deals (Bloomberg)

Podcasts & Interviews

Ares’ co-head of alternative credit (Joel Holsinger) says AI will hit a bit of a wall due to ‘sheer capital’ (Credit Exchange)

Former Goldman Sachs CEO Lloyd Blankfein Says the Market Is Due for a Reckoning (Bloomberg)

Ramp founder Eric Glyman on the many ways AI is changing corporate spending (Cheeky Pint)

The Three Main Verticals of ABF with Missy Dolski of Varde Partners (Credit Clubhouse)